By Steve Pomeroy

Over the recent years, many Canadian cities have seen significant inflation in home prices, raising concerns about the ability our young first-time buyers to get onto the home ownership ladder.

There is some debate as to whether this is a result of a lack of supply or a result of excessive demand. Of course, both contribute to this phenomena but it’s important to better understand the respective contributions before we can start to identify possible solutions. This is the second of a three part blog to explore these issues. Blog 1 first examined the case for insufficient supply; thus Blog 2 examines the role and nature of demand. Blog 3 subsequently concludes with a discussion of some policy options.

Part 2: How demand drives up prices

Part 1 sought to dispel the myth that the main cause of home price escalation in Canada is from undersupply. Here this is complemented by examining the demand side and the pattern of price rises compared against the capacity of households to buy. This analysis examines how a combination of declining and low mortgage rates combined with upper middle class incomes and substantial levels of accumulated equity combine to create super-charged purchasing power and is a key factor in driving up home prices.

The phenomenon of rising home prices has been experienced across all centres, some more than others, in particular in the large metropolitan regions of the GTA and Vancouver. The fact that this phenomenon is widespread suggests there are common causes all across the country. These reflect the fundamentals of how many, and which type of households seek to purchase, what are their income and what is their capacity to carry mortgage costs.

Over the last 20 years there has been a steady decline in mortgage interest rates, which have extended the reach of households with increasing incomes (Exhibit 1).

The pattern of price increase is shown at an aggregate national scale using MLS home sale prices against the increased leverage capacity (Exhibit 2).[1] That is, how much mortgage can the median couple household (predominant buyers) afford at the prevailing interest rate and their current income.

Using national aggregate data (details for selected cities are examined later) Exhibit 2 shows that until 2021 the potential mortgage capacity exceeded the median home price – suggesting that on average, there is reasonable alignment between prices and capacity to pay, among median income couple families (and many buyers may be above median income and thus have even greater capacity).

This reflects only mortgage capacity; if down payment amounts, highlighted below, are added, the affordable price level would increase – and this is especially so for move-up buyers bringing their accumulated equity with them.

As the last statement implies, in undertaking this analysis it is also important to consider who the buyers are. Less than one third are first time buyers (FTBs)[2]; over two-thirds are repeat or move-up purchasers that have accumulated equity from existing property to contribute as part of the purchase. And some of these are investors, also leveraging their existing assets.

Leaving aside investors, the vast majority of purchasers are households with two incomes. So, its more relevant to use the incomes of two income families.[3] It is also helpful to quantify the nature of recent sales prices. There are just over 14 million households in Canada (and just under 10 million already own); home sales in any one year (including MLS existing plus CMHC new homes) have averaged around 700,000 annually over the last few years.

So, in any one year, only 5% of households are active and responsible for the market outcomes. And only one quarter of all buyers and 1% of all households are first time buyers. This relatively small number of market participants is skewed toward higher income (especially two income families) and those with accumulated equity, a windfall gain from rising home prices.

It is this very small number of households that are responsible for activity in the home resale market. These are predominantly existing owners (recall fewer than one third, or 200,000 are FTBs) that have both strong income and considerable amounts of accumulated equity. Given these income and equity characteristics, this small group of “supercharged” purchasers exert substantial influence on the trajectory of home prices – while many bystanders lack the income or equity to participate in the market.

So, it is not the quantity of buyers (i.e. total demand, from household growth and immigration) it is the quality (incomes, and wealth, abetted by low mortgage rates) of this very small segment of “market makers” that have been the ones driving up home prices.

Investor buyers are also a part of this, and speculative activity is heightened in periods of strong price gains, further exacerbating the price trend.

If policy makers wish to address excessive price increases, they must target this small, identifiable group of “supercharged market makers” and introduce appropriate constrains on their ability to drive the market.

Before discussing the policy implications and options to address this issue, a demand analysis is presented for a cross-section of cities to show that it is playing out in a number of markets, although there may be additional factors in Vancouver and the GTA.

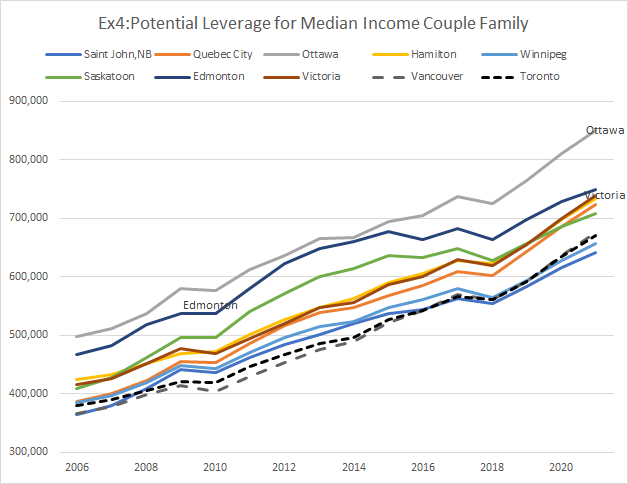

There is a parallel pattern of both rising prices (Exhibit 3) and rising leverage (Exhibit 4, potential mortgage leverage) across most cities.[4] Cities with higher median couple incomes, for example Ottawa, have the greatest leverage impact, and counter-intuitively, in the more expensive cities of Vancouver and Toronto a lower median income reduces leverage capacity.

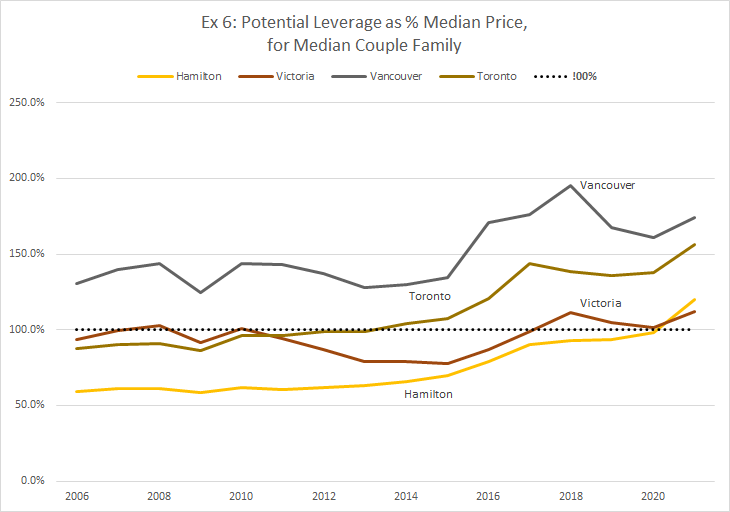

Examining how these incomes and prices interact, Exhibits 5 and 6 present the median home price as a percentage of the leverage capacity for each city.

As illustrated in the Canadian composite earlier, in most cities, the capacity to pay (mortgage leverage) has over the last 15 years substantially exceeded the actual median price (the price: leverage ratio is well below 100% for cities in Exhibit 5).

In some cities, the leverage ratio has actually declined (i.e. ownership is more affordable to the median household, see Ex 5). Ottawa, which has one of the highest median couple incomes in the country, has seen this quality of demand pull home prices higher, reinforced by strong quantity of demand (historically high levels of immigration, primarily domestic, and including people cashing out of Toronto). But prices in Ottawa still remain below 80% of capacity – for the median couple family, who are likely to pull them up further, especially if incomes continue to strengthen and interest rates remain low.

Exhibit 6 presents the data for the major centres of Vancouver and Toronto and nearby, Victoria and Hamilton, both impacted by spillover demand from the larger metro cities. Here the leverage effect falls well short of actual median home price and this is not a new phenomenon. Across the period since 2005, the price-to-leverage ratio in Vancouver has been well above capacity to pay and since 2016 above 150%; prices are more than 50% above what the median income household can afford. In Toronto, the issue is not quite as extreme, but even here, the ratio crossed 100% in 2014 and moved above 150% in 2020.

More recently (2020), both Victoria and Hamilton have also moved above the 100% threshold.

In each case the median income couple household can afford the median priced home, only if they have a large down payment, in the cases of Vancouver and Toronto a down payment of more than one-third of the price. But as suggested above by the small proportion of FTBs, the primary purchasers are drivers of the price trajectory are the super-charged repeat buyers and investors. They have this high level of equity because, depending when they originally got in to the local market, they have ridden the wave of rising prices to a windfall gain and now have substantial accumulated equity to enable buying at these much higher prices.

Anecdotal, and some more recent statistical evidence suggests that foreign buyers may also be more of a factor in Vancouver and Toronto, than in other cities but while tending to target higher value homes, in absolute terms these buyers represent only a small fraction of purchasers.

The main driver is domestic buyers, both those cashing out of higher priced markets (causing high bids in places like Victoria and Hamilton) or from local move up buyers and investors who are enabled by accumulated appreciation.

Policy implications

This analysis asserts that it is not the quantity of buyers (i.e. total demand, from household growth and immigration) that is driving up home prices; rather, it is the quality (incomes, and wealth) of this small segment of “market makers” that is making the difference.

This small segment is creating a market imbalance and serious challenge for lower income households (including single income lone parents and singles) and especially those that rent and have not benefitted from the windfall gain of appreciating home equity.

If the issue were one of too many buyers (excess quantity of demand), then an increase in supply could be an effective way to moderate the price increases. And with rising levels of international migration, there is a need to expand supply, and starts data suggest the market is already responding.

But adding supply alone will not address the issue highlighted here – the excessive capacity to pay. Given this capacity and related demand, builders continue to construct detached or semi-detached homes and price these at levels that this small segment of buyers can readily afford (given both their higher income as well as accumulated equity).

So, adding supply, even in high volume, will not necessarily stall or reduce prices. And accelerating municipal approvals, as advocated by many in the industry, and in the election platforms, may simply move the pressure to elsewhere in the supply chain. With limits on labour, land and materials (e.g. rapid rise in lumber costs), this may have the unintended effect of increasing prices, and worsening affordability.

Separate from any supply response, the key is to contain or suppress this excessive demand capacity, which is driven in large part by low mortgage rates and by accumulated appreciation. These options are examined in part 3.

[2] Explicit data on the share of FTBs is elusive. However recent data from the Canada Housing Statistics Program (CHSP) provides some insight. It identifies the number of households in 2018 that claimed the Home Buyer Tax credit on their tax return. Comparing this number against the CREA statistics on total home sales (may undercount as this excludes exclusive sales and direct sales by builder/developers) for NB, Ontario and BC suggests that fewer than 30% of sales were to FTBs. And in all cases the median income of FTBs was higher than that of existing owners, suggesting is in predominantly young couples with two good incomes (and possible some down payment assistance from parents).

[3] Nationally, couples median income is 109% of overall median; incomes of lone parent and single person households are much lower at 56% and 34% respectively. However it is the two income couples that most influence the market, representing over 80% of all purchases (Statistics Canada, CHSP 2019)

[4] Notably home prices in a number of Prairie cities, especially in Alberta, have not followed the price trend, mainly because of weak demand following the collapse of the oil sector economy and reversal of inter-provincial migration.

Your analysis is very interesting. The basics of house pricing is: desirability, supply, and affordability. I had not thought about the accumulation of equity as an ability to pay more. but of course the more you can transfer to the next house coupled with low mortgage rates really can multiply your capacity to pay more.

I am active in buying, renovating, and selling in both Canada and the US so I have a more than passing interest in housing prices and look forward to part three.